Cost Sharing Explained: Deductibles, Copays, and Coinsurance for Medications and Care

When you fill a prescription for your diabetes medication, you hand over your insurance card and a $25 bill. That’s a copay. But later, you get a bill for $300 for a specialist visit and lab work. You’ve already paid $1,200 this year for doctor visits and meds. Now you’re wondering: Why am I still paying so much? That’s where deductibles and coinsurance come in. Most people don’t understand how these three pieces fit together - until they’re hit with a surprise bill. And if you’re managing a chronic condition like high blood pressure, asthma, or rheumatoid arthritis, not knowing the difference can cost you hundreds - or thousands - of dollars a year.

What Is Cost Sharing, Really?

Cost sharing is the part of your medical or medication bill that you pay yourself. Your insurance doesn’t cover everything. Even if you pay $500 a month for your plan, you’re still responsible for a chunk of each visit, test, or pill. This isn’t a loophole - it’s by design. The idea is simple: if you pay something, you’re less likely to use care unnecessarily. But for people with ongoing health needs, this system can feel like a maze.The Affordable Care Act (ACA) made sure every plan sold on the marketplace clearly defines three types of cost sharing: deductibles, copays, and coinsurance. These are the only three ways your insurance shares the cost with you. Everything else - like your monthly premium or charges for services your plan doesn’t cover - doesn’t count toward your out-of-pocket limit.

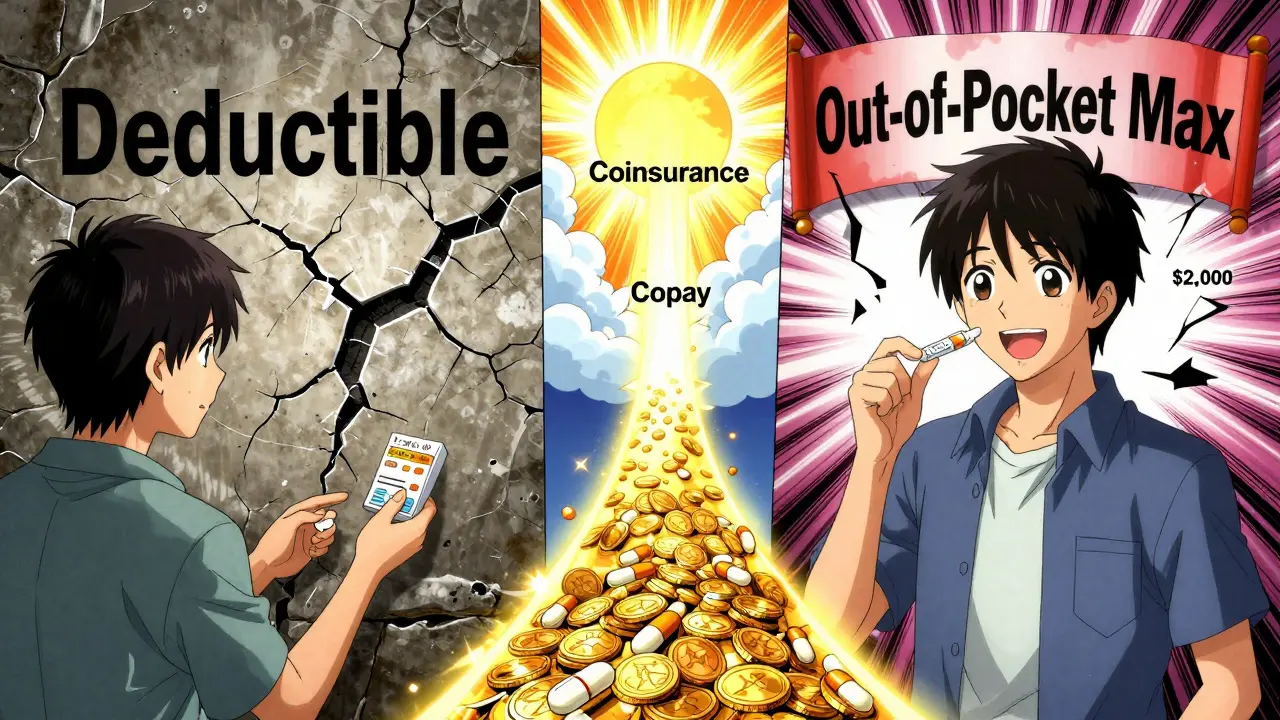

Deductibles: The First Hurdle

Your deductible is the amount you pay out of pocket before your insurance starts helping with most services. Think of it like a bucket. You fill it with every dollar you spend on covered care - doctor visits, lab tests, hospital stays, and prescriptions. Until that bucket is full, you pay 100%.For example, if your plan has a $2,000 deductible, you pay the full cost of your blood pressure medication ($120), your annual physical ($150), and your MRI ($800) until you’ve spent $2,000 total. Only then does your insurance start paying part of the bill.

But here’s the twist: not everything counts toward your deductible. Preventive care - like flu shots, mammograms, or annual check-ups - is usually free, even before you meet your deductible. That’s thanks to the ACA. So if you’re healthy and only need one or two visits a year, you might never even touch your deductible.

High-deductible plans (HDHPs) are becoming more common. In 2023, the average deductible for an individual was $1,945 - up from $1,170 in 2010. These plans often come with lower monthly premiums, which can be tempting. But if you take multiple medications or see specialists regularly, you’ll hit that deductible fast - and then you’ll still owe coinsurance.

Copays: Fixed Fees at the Point of Care

A copay is a flat fee you pay when you get care. It’s usually due right then and there - at the pharmacy counter, the doctor’s office, or the ER. Copays are predictable. You know exactly how much you’ll pay.For prescriptions, copays vary by tier:

- Generic drugs: $10-$20

- Brand-name drugs: $40-$75

- Specialty meds (like biologics for arthritis): $100-$500

Some plans charge a copay even before you meet your deductible. Others require you to pay the full price until your deductible is met, then switch to a copay. This matters a lot if you’re on a specialty medication. For example, a rheumatoid arthritis drug might cost $6,000 a month. If your plan requires you to meet your $7,000 deductible first, you’re on the hook for the full $6,000 - until you hit that number. Then your copay drops to $150. That’s a huge difference.

One common mistake? Assuming your copay is the same for every drug. It’s not. Your plan has a drug formulary - a list of covered medications ranked by cost. The higher the tier, the more you pay. Always check your plan’s formulary before starting a new med.

Coinsurance: The Percentage You Pay After the Deductible

Coinsurance kicks in after you’ve met your deductible. It’s not a fixed amount - it’s a percentage. If your plan says you pay 20% coinsurance, you cover 20% of the cost of each covered service, and your insurance covers the other 80%.Let’s say your insulin costs $300 per month. After you hit your $2,000 deductible, your coinsurance is 20%. That means you pay $60 a month. Your insurance pays $240. But here’s what people forget: that $300 is the allowed amount your insurer negotiated with the pharmacy. If the pharmacy charges $400, you still only pay 20% of $300 - because that’s what your plan considers “reasonable.”

Coinsurance applies to everything after your deductible: specialist visits, lab work, hospital stays, and prescriptions. It can add up fast. If you need a surgery that costs $15,000 and your coinsurance is 20%, you owe $3,000. That’s not a copay - that’s a big bill.

And coinsurance doesn’t stop at the deductible. It continues until you hit your out-of-pocket maximum.

The Out-of-Pocket Maximum: Your Safety Net

This is the most important number you need to know. Your out-of-pocket maximum is the most you’ll pay in a year for covered services - including your deductible, copays, and coinsurance. Once you hit it, your insurance pays 100% of everything else for the rest of the year.In 2023, the ACA capped this at $9,100 for individuals and $18,200 for families. That means if you’re on a high-cost medication like Humira or Enbrel, and you’ve paid $9,100 in deductibles, copays, and coinsurance, your next prescription - no matter how expensive - is free.

But here’s the catch: premiums don’t count toward this limit. So if you pay $600 a month in premiums, that’s $7,200 you’re paying on top of your out-of-pocket costs. That’s why some people with chronic conditions end up paying more than the out-of-pocket maximum - because they’re paying premiums and out-of-pocket costs.

How These Three Work Together

Imagine you’re on a plan with:- $3,000 deductible

- $40 copay for primary care

- 30% coinsurance after deductible

- $8,000 out-of-pocket maximum

January: You get a blood test. Cost: $200. You pay $200 (deductible).

February: You see your doctor. Copay: $40. You pay $40 (deductible).

March: You refill your asthma inhaler. Cost: $120. You pay $120 (deductible).

April: You need an MRI. Cost: $1,500. You pay $1,500 (deductible).

Now you’ve paid $1,860 toward your $3,000 deductible. You still owe $1,140.

May: You get a specialist visit. Cost: $400. You pay $1,140 (to finish deductible), then 30% of the remaining $260 = $78. Total: $1,218.

June: You refill your specialty medication. Cost: $800. You pay 30% = $240.

By November, you’ve paid $7,900 total toward your out-of-pocket max. In December, you need another expensive test: $2,000. You pay $100 (because $7,900 + $100 = $8,000). That’s it. The rest of the year, everything is free.

What You Can Do Today

Don’t wait until you’re hit with a $5,000 bill to understand your plan. Here’s what to do now:- Find your Summary of Benefits and Coverage (SBC). It’s required by law. Look for the section on “Cost Sharing.” It will show examples like: “If you have a broken leg, here’s what you’d pay.”

- Check your drug formulary. Search your meds by name. See what tier they’re on and what your copay is.

- Call your insurer. Ask: “If I fill my medication today, how much will I pay? Is it a copay or coinsurance? Has my deductible been met?”

- Use your insurer’s online cost estimator. Most have tools that show you how much a service will cost at different locations - in-network vs. out-of-network.

- Ask about patient assistance programs. Many drugmakers offer discounts or free meds if you qualify based on income.

And if you’re on Medicare? Insulin is capped at $35 a month. That’s a game-changer. Check if your plan includes this.

Common Mistakes That Cost People Money

- Thinking your copay counts toward your deductible. It doesn’t - unless your plan says so. Most plans require you to pay full price until the deductible is met.

- Assuming all prescriptions are covered. Some plans don’t cover certain brands or require prior authorization.

- Ignoring out-of-network charges. Going to a pharmacy or doctor outside your network can double your coinsurance - or make you pay 100%.

- Forgetting about the out-of-pocket max. Once you hit it, you’re done paying. But you have to track your spending.

One patient in Pittsburgh told me she paid $1,800 for a single medication because she didn’t realize her deductible hadn’t been met. She thought her $50 copay was all she’d ever pay. That’s not rare. The Patient Advocate Foundation found that 31% of people with chronic conditions got hit with surprise bills because they didn’t understand coinsurance.

Final Thought: Know Your Plan Like Your Medication Schedule

You don’t forget to take your pills. Don’t forget to know your plan. Cost sharing isn’t just fine print - it’s your financial lifeline. Whether you’re on a high-deductible plan to save on premiums, or a platinum plan to avoid big bills, you need to know exactly where you stand.Ask questions. Track your spending. Use your insurer’s tools. And if you’re overwhelmed, call a patient advocate - many hospitals and nonprofits offer free help.

Because when it comes to your health, you shouldn’t have to choose between paying for meds and paying rent. Understanding cost sharing is the first step to taking control.

What’s the difference between a deductible and a copay?

A deductible is the total amount you pay each year before your insurance starts helping with most services. A copay is a fixed fee you pay at the time of service - like $30 for a doctor’s visit - and it may or may not count toward your deductible, depending on your plan.

Do copays count toward my out-of-pocket maximum?

Yes, copays almost always count toward your out-of-pocket maximum. So do your deductible payments and coinsurance. But your monthly premiums do not. Once you hit your out-of-pocket max, your insurance pays 100% of covered services for the rest of the year.

Why do I pay more for some medications than others?

Your plan puts medications into tiers. Tier 1 is usually generic drugs with the lowest copay. Tier 2 is brand-name drugs. Tier 3 and 4 are specialty meds - often for chronic conditions - with the highest cost. The higher the tier, the more you pay. Always check your plan’s formulary before starting a new drug.

Can I avoid coinsurance?

You can’t avoid coinsurance if your plan uses it - but you can minimize it. Use in-network providers, choose generic drugs when possible, and ask your doctor if there’s a lower-cost alternative. Also, once you hit your out-of-pocket maximum, coinsurance stops. So if you’re on expensive meds, keep tracking your spending - you might be closer to free care than you think.

What happens if I go to an out-of-network pharmacy?

You’ll likely pay more - sometimes a lot more. Your plan may only cover a portion of the cost, or it may not cover it at all. Coinsurance could jump from 20% to 50% or higher. Always use in-network pharmacies. If you must use an out-of-network one, call your insurer first to find out what you’ll owe.

Is there help if I can’t afford my meds?

Yes. Many drug manufacturers offer patient assistance programs that give free or discounted meds to people with low income. Nonprofits like NeedyMeds and the Patient Advocate Foundation can help you apply. Medicare beneficiaries also get insulin capped at $35/month. Check your eligibility - it’s easier to get help than you think.

Kerry Howarth

January 2, 2026 AT 00:33Just read your SBC last week. Found out my insulin copay was $35 because of the Medicare cap. Didn't know it applied to me until I called. Game changer.

Stop assuming your plan works the same as everyone else's.

Joy F

January 3, 2026 AT 01:52Let’s deconstruct the neoliberal architecture of healthcare cost-sharing, shall we? The deductible isn’t just a financial barrier-it’s a biopolitical mechanism designed to extract surplus value from the chronically ill while masquerading as fiscal responsibility. Coinsurance? A psychological weapon. Copays? The performative illusion of affordability. The out-of-pocket max? A mirage. Premiums are the real tax. And don’t get me started on formularies-they’re corporate cartels disguised as clinical guidelines. We’re not patients. We’re revenue streams with pulse rates.

And yes, I’ve been on Humira for 7 years. I know.

Haley Parizo

January 4, 2026 AT 04:33You think this is about money? It’s about power. The system doesn’t want you to understand this because understanding means you can fight back. They need you confused, exhausted, and quietly paying. The moment you track your out-of-pocket spending, you become a threat. That’s why they bury the SBC in a PDF no one reads. That’s why they don’t send reminders. That’s why your pharmacist doesn’t tell you about patient assistance programs unless you ask-twice.

Stop being a consumer. Start being a warrior. Your life depends on it.

Ian Detrick

January 4, 2026 AT 10:13This is the kind of post that should be required reading for every high school senior before they pick a health plan. I wish I’d known this at 22 when I picked the ‘cheap’ plan and ended up paying $4k for a broken ankle.

Knowledge is power, but in healthcare, it’s survival. Bookmark this. Print it. Tape it to your fridge.

Angela Fisher

January 5, 2026 AT 12:02Okay but what if the whole thing is a scam? Like... what if insurance companies and pharma are in cahoots? I read this one Reddit thread where a guy said his drug price went up 300% after he hit his deductible because the insurer 'reclassified' it. And the formulary? Totally rigged. They put the expensive stuff on tier 4 so you have to pay more and they make more off your suffering. And don't even get me started on the ER bills-those are designed to break you. I think they use AI to predict who's gonna break first and then hit them with the worst bills. I swear, I saw a billboard that said 'Your Health Is Our Priority' and I cried. I'm not even joking. 😭

They know we're desperate. And they're laughing.

Also, my cousin got charged $12k for a CT scan that was supposed to be 'covered.' He had to sell his car. I'm not okay.

Someone please tell me I'm wrong. I need to believe this isn't intentional.

Neela Sharma

January 5, 2026 AT 15:01When I came to the US from India with asthma, I thought my inhaler was expensive at ₹800

Then I saw the price tag in dollars

Then I learned about deductibles

Then I cried in a pharmacy aisle

Now I call my insurer every month like it’s my job

Because if I don’t, I pay twice

And I can’t afford to pay twice

But I do anyway

Because what choice do I have?

Still, I thank you for writing this

It’s the first time I felt seen

Not as a patient

But as a person trying to survive

Liam Tanner

January 6, 2026 AT 04:33Biggest tip I’ve learned: Always ask the pharmacist, ‘Is there a generic alternative that’s covered?’

They’re not supposed to push it, but if you ask nicely, they’ll often say yes.

Also, never pay cash unless you’ve checked your insurer’s price first. Sometimes the cash price is lower than your coinsurance. Crazy, right?

And yes-call your insurer. Even if you think they won’t help. They will. Sometimes.

Palesa Makuru

January 6, 2026 AT 12:43Oh honey, you think this is bad? Try living in a state that didn’t expand Medicaid and having a kid with cystic fibrosis. You pay your premium, you pay your deductible, you pay your coinsurance, you pay for the special formula, you pay for the nebulizer, you pay for the transport to the clinic, you pay for the parking, you pay for the babysitter so you can go to the clinic, you pay for the emotional toll, you pay for the sleepless nights, you pay for the guilt of not being able to afford the new drug that could extend your child’s life by six months.

And you still have to explain to your boss why you’re late again.

So yes, your $25 copay is a luxury. I’m jealous.

Hank Pannell

January 7, 2026 AT 10:02Let’s talk about the cognitive dissonance baked into this system. We’re told to be ‘responsible consumers’ of healthcare, yet the pricing is intentionally opaque. We’re encouraged to ‘shop around’ for services, but the data is locked behind proprietary portals. We’re told coinsurance is ‘fair,’ but it scales with inflation while wages stagnate. And yet, the same people who preach ‘personal responsibility’ never mention that the out-of-pocket max doesn’t include premiums, which are rising faster than any other cost.

It’s not a system designed to help. It’s a system designed to extract. And the ‘help’ they offer-patient assistance programs-requires paperwork, income verification, and emotional labor most of us are too exhausted to muster.

So yes, track your spending. Yes, call your insurer. But also-demand systemic change. Because no amount of personal finance hacking should be required to stay alive.

Sarah Little

January 8, 2026 AT 19:47Just want to clarify something: copays for specialty meds often don’t count toward your deductible unless your plan explicitly says so. I learned this the hard way when my rheumatoid arthritis drug was $1,200/month and I thought my $150 copay was ‘helping.’ It wasn’t. I had to pay full price for 11 months before the deductible kicked in. Then the coinsurance hit. Then I hit the max. Then I got a letter saying ‘thank you for your loyalty.’

Read your plan. Like, actually read it. Not the summary. The full document. It’s 87 pages. I know. I’ve read it three times.

innocent massawe

January 8, 2026 AT 21:53From Nigeria, I just want to say thank you.

Here, if you can’t pay, you don’t get care.

You don’t have deductibles.

You have death.

So when I read this, I cried.

Not because I understand it.

But because I wish we had this mess.

At least here, you can fight it.

Here, you just die.

Thank you for writing this.

🙏

veronica guillen giles

January 9, 2026 AT 02:11Wow. A post about healthcare that doesn’t end with ‘just call your provider.’

Who wrote this? A saint? A martyr? A former insurance rep who had a crisis of conscience?

Either way, I’m printing this and putting it in my husband’s insulin box.

Because if he dies from not knowing this, I’m suing the entire American healthcare system.

And I’ll bring snacks to the courtroom.